Our current System is undergoing a massive shock, and the heroes within our essential services are to be lauded for their dedication. The lessons they are being subjected to should not be forgotten.

While we come to terms with the impact on our daily lives and the enormous strains on the people managing our overloaded resources, the speed with which we are able to respond is a major factor in near-term outcomes.

In the longer term, I wonder what a world should look like in 5, 10, 15 years from now, if the System became able to more easily manage and adjust to shocks such as these – and how integrating AI and ML, ESG, tokenomics, block chain smart contracts and even gamification would reboot and prepare the System to reduce the turmoil. Can a distribution theory lead to a more balanced and fair System for all, no matter who or where we are?

From 2007 onwards, Nassim Nicholas Taleb published a series of philosophical books (Fooled by Randomness, The Black Swan, The Bed of Procrustes, Antifragile, and Skin in the Game). These books and their theories minutely examined and explained:

- humans’ fallible knowledge mechanisms

- the innate human ability to detect patterns that lead us to mistakenly identify them where there are in fact none – when there are no actual causal linkages between the events we are observing with negative consequences

- conversely, that having ‘skin in the game’ (for example, by a fund manager), protects the investor against irresponsible trading

In dealing with Systemic Shock he essentially advocates a society that can withstand events that have far-reaching impacts; that blur boundaries between political, health, economic and environmental spheres. Our question should, therefore, be: “how” should the world’s System change to mitigate against such shocks?

In the world of due diligence and investing, (where we are aiming to make an impact), the general thesis of investing must push well beyond the boundaries of economic gain and deep into the ESG arena. This is a well posited argument from economists such as Kate Raworth, to name one of many. Investment managers are programmed to detect patterns in events for survival purposes. Even the most expert, experienced and highly educated investment professionals show an alarming natural tendency to apply bias and to see “false” patterns in historic events and data, and then to base future predictions and scenario modelling on these non-existent causative inferences.

Taleb’s writings clearly demonstrate the perilous folly of this, using it to explain why, time and again, humans (and markets) are blindsided by unexpected events that fall beyond the predictive scope of these flawed patterns. These are not subtle shifts: they have vast magnitude and consequence. Yet, even when an event has already proven to have been deleterious on a large scale, our congenital biases prevent us from accurately observing uncertainty and even from recognising its impact. It’s the reason why historical myths persist when research has already proven them to be incorrect: they fit the pattern that our unconscious minds wish to see, while the real causes fall into our blind spot.

Blinded by, and vulnerable through, our own survival expertise?

We are effectively blind to randomness, and particularly susceptible to large, high-profile rare events that are wholly outside of our normal realm of expectation. Given the huge historical impact of these events (the World Trade Centre attack is another perfect example), this blindness can be catastrophic, as evidenced by the massive effect of the Coronavirus on countries’ infrastructure and healthcare systems with the psychological fallout resulting in panicked decision-making and, of course, the disastrous effect of all of this in the investment realm. Taleb constantly reiterates that banks and trading firms are especially vulnerable to perilous events, as their entire approach forces them to become hugely exposed to losses that cannot be predicted by their financial models. A further lack of “skin in the game” by banks and trading firms leaves investors carrying the burden of the flawed models imposed on them.

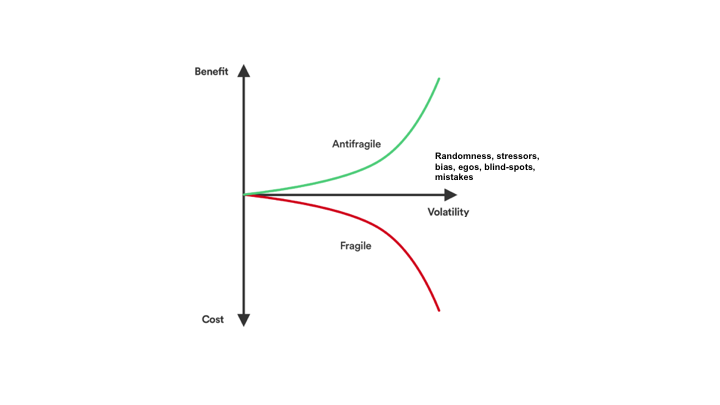

“Antifragility” – an antidote to the viral effect of shock events?

All of which leads to a “solution” posited by Taleb, and since adopted in a wide variety of fields, from risk analysis to transportation planning, IT and space flight planning. The primary tenet is to move away from the idea of trying to predict a System shock, and rather to insulate oneself from the negative instances, while remaining open enough to the impact of positive ones so as to be able to extract benefit when similarly, unexpected, vastly catalytic opportunities present themselves. Anything that has more upside than downside from random events (or certain shocks) is “antifragile”; the reverse is fragile.

Compounding investment intelligence to become “antifragile”

Although absolutely nothing has changed about our evolutionary programming since Taleb’s publications, what has changed is the technology we now have at our disposal to become more “antifragile”. Using innovative cloud computing to combine swarm intelligence with collective investment, we are able to create a living, breathing system that can respond organically to unpredictable events and use them to our advantage, rather than working off a rigid centralised (and flawed) predictive analysis model or pattern simulation. This is the exact type of advancement we need in order to become antifragile. An example of this more decentralised model is how Folding@home (a distributed computing initiative tasked with developing therapies for disease) revealed their latest project: “a coronavirus-centric research effort harnessing a global computer network. The project aims to use the combined computing power of thousands of people around the world to formulate pharmaceutical drugs in the combat against the coronavirus”. In a matter of weeks, they have been able to harness the computing power of over 400,000 computers.

Democratising venture capital

The use of technology-driven swarm intelligence feedback and collective insights at all stages of investment analysis, would aim to empower participants by enabling better decision-making and greater investment capability for all. Deep market research and distributed due diligence is the way to mitigate investing risks by future proofing the investment process. A distributed high-risk thesis is needed to reboot the System with support for impactful ideas that build resilience and antifragility, and investors need to take a Whole System approach.

Modelling platforms on this distribution thesis creates a plausible (not predictable) solution through a network effect – intelligent distributed due diligence, and collective allocation of resources. It’s a digital solution that combines the power of technology with the expertise of the network to reach collective consensus and investment in ventures not for the sake of only economic gain, but also being cognisant of planetary, social and governance boundaries. This allows for unbiased decision-making, digitised due diligence and governance, and uncompromised investment democracy. The beauty of this is the lack of constraint of an organisation – the power is in the network.

To enhance the system another step, there should be a “skin in the game” imperative throughout the process. The System should be developed even further: there is tangible momentum behind the inclusion of sustainability-focused funds in portfolios, driven by sustainable development goals and associated sustainability narratives, regulatory pressure – and simply because it’s good for business. Rapid changes are continuing to take place in the industry, in ways which are still not clearly defined, and in which a variety of approaches and strategies are needed to correspond with diverse expectations and needs of investors. A perfect example is fractionalisation through platform technology, which spreads risk across many investments and returns among many investors.

Finally, a particular commodity that is becoming increasingly valuable is trust. Increased regulation has been the traditional approach to preservation of trust and to ensure emergence of good practice. It is now increasingly important for disclosed company information to be not only accurate and clear, but reliable and not misleading.

By taking such a Whole System approach and incorporating the lessons from Taleb’s theses, we can begin to create an investment environment that is antifragile – not only capable of withstanding system shocks, but of using them to develop and thrive.